IASBは、IFRS10号「連結財務諸表」の規定が免除される企業として「投資企業」を定義する改正案を、8月25日に公表しました。

The International Accounting Standards Board (IASB) published today proposals to define investment entities as a separate type of entity that would be exempt from the accounting requirements in IFRS 10 Consolidated Financial Statements.

投資企業とは、一般に、幅広い投資家から投資目的のみで投資を集めている企業と理解されています。IFRS10号「連結財務諸表」においては、投資企業が投資先の企業を支配している場合には、連結することが求められています。しかし、IFRS10号制定の際に、これでは、投資の価値を評価するのに必要な情報が提供されないという投資家からのコメントがありました。この問題に対応するために、今回の公開草案では、「投資企業」に該当するために満たさなければならない規準を定めています。このような企業は連結規定が免除されますが、その代りに、すべての投資を公正価値で評価し、評価差額を損益計上しなければなりません。公開草案は、投資の性質や種類に関する開示についても規定しています。

Investment entities are commonly understood to be entities that pool investments from a wide range of investors for investment purposes only. Currently, IFRS 10 Consolidated Financial Statements would require consolidation if an investment entity controls an entity it is investing in. However, when developing IFRS 10, investors commented that this would not provide them with the information they need to assess the value of their investments. To address this issue, the exposure draft published today proposes criteria that would have to be met by an entity in order to qualify as an investment entity. These entities would be exempt from the consolidation requirements and instead would be required to account for all their investments at fair value through profit or loss. The exposure draft also includes disclosure requirements about the nature and type of these investments.

このプロジェクトは、IASBと米FASBの共同で行われているものです。両者の案はほぼ同じものですが、FASBは、投資企業が、投資企業でないより大きな企業グループによって所有されている場合にまで免除を拡大適用する案を検討しています。

This project is being undertaken jointly by the IASB and the US national standard-setter, the Financial Accounting Standards Board (FASB). Both boards’ proposals are broadly aligned. However, the FASB is considering proposing that the exemption would extend to cases in which the investment entity is owned by a larger group that is not itself an investment entity. The FASB will publish its exposure draft in due course.

投資会社について例外を認めるというのは、日本のいわゆるベンチャーキャピタル条項に似ていますが、連結しないで原価で計上するというのではなく、毎期投資先を時価評価するという点ではまったく異なります。

もっとも投資企業の要件の中に「公正価値マネジメント」(投資を時価で管理していること)というのがあります。もともと時価評価しているはずだというのが前提となっているようです。

Substantially all of the investments of the entity are managed, and their

performance is evaluated, on a fair value basis [‘fair value management’].

公開草案はこちら↓

Exposure draft on investment entities [Aug 2011]

IASBによる簡単な解説↓

Snapshot: Investment Entities(PDFファイル)

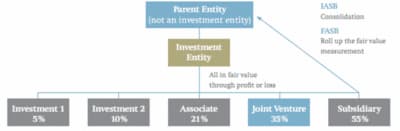

今回の案およびFASB案との差異を説明した図

この図をみると、子会社(Subsidiary)ではあるが連結からは除外ということになります(「子会社」から除外するのではない?)。

(補足)

2011.08.25 国際会計基準審議会(IASB)が、公開草案 「投資会社」を公表(トーマツ)

IASB、公開草案「投資会社」を公表(あずさ)